President Trump has recently escalated his long running criticism of Fed Chair Powell, lambasting him for keeping interest rates too high and accusing him of “playing politics”. He lamented that “Powell’s termination cannot come fast enough!” and warned, “If I want him out, he’ll be out of there real fast, believe me.”1

Attempting to fire Fed Chair Powell would test the legal safeguards that protect the Federal Reserve from political pressure. Most likely, it would also destabilise financial markets, as highlighted by Treasury Secretary Bessent.2

Yet President Trump seems happy to flirt with the idea of firing Powell before his term as Chairman ends in May 2026. However, many commentators note that the attempt to remove Powell would face serious legal challenge.

The legal background

The Federal Reserve Act sets clear limits: Under 12 U.S.C. paragraph 242, the President may remove a Fed governor or chair only “for cause”. Courts have long held that “cause” means misconduct or incapacity and does not apply to differing views on policy. This suggests that any attempt to dismiss Mr Powell on those grounds would collapse under legal scrutiny.

Another safeguard for the Fed’s independence is the 1935 Supreme Court decision in Humphrey’s Executor v. United States. That ruling established that Congress may insulate officials of independent agencies from removal except for “inefficiency, neglect of duty, or malfeasance in office.” Fed governors and chairs have relied on this decision for protection.

However, Mr Trump’s legal team is seeking to strip similar “for cause” protections from the National Labor Relations Board and the Merit Systems Protection Board. They argue the President cannot be constrained in shaping his executive team. The Supreme Court decisions on these cases could reshape the contours of agency independence, including that of the Federal Reserve.

That the Fed sets monetary policy independently has historically been a cornerstone of financial system stability. The US Congress granted the central bank this status to ensure that it could set policies affecting the economy and banking system free from political interference. Indeed, the financial community as well as members of both parties in Congress see an independent Fed as vital to preserving a strong economy.

Likely market impact

Investors value stability and predictability highly. If Chair Powell were fired it would likely prompt a violent reaction against US assets, encouraging money to flee abroad.

Waning confidence in the Fed’s resolve to curb inflation could lead bondholders to demand an increased risk premium to hold Treasuries, pushing up medium-to-long dated bond yields. As a counterexample of what could happen to bond yields if the Fed’s independence is diminished is the market reaction to the Bank of England unexpectedly becoming independent in 1997. Several authors have documented how UK inflation expectations and bond yields fell, and long-term inflation expectations became less sensitive to the current state of the economy.3

As short-term rates would be expected to be cut aggressively under a new Trump-appointed leadership, the US yield curve would steepen dramatically, although that would not necessarily signal an improved growth outlook. Any attempt by the Fed under the new chair to limit the surge in yields, for instance by restarting quantitative easing, would likely be met with even stronger selling flows by private and international investors.4

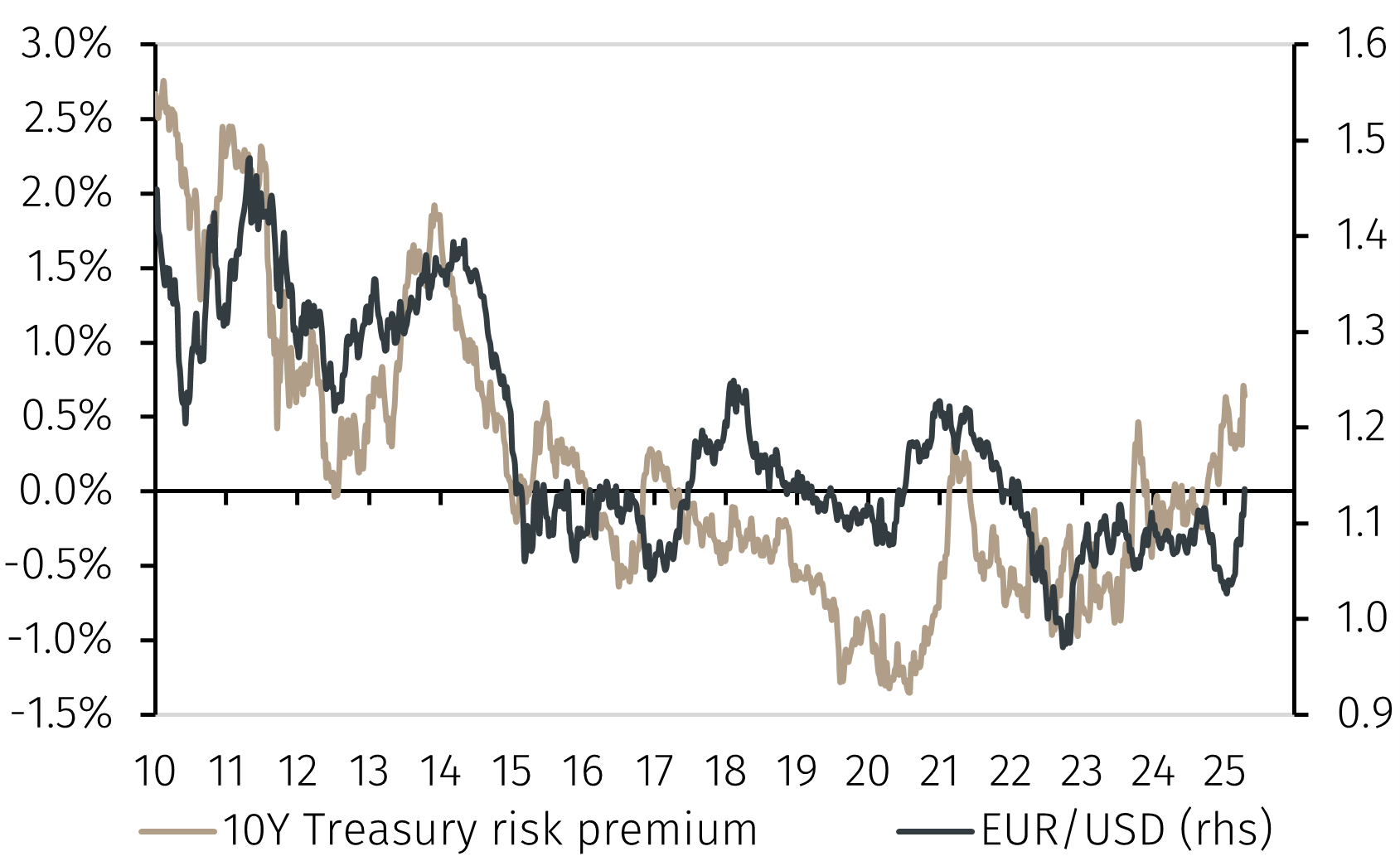

The US dollar would also be negatively impacted. Its role as the world’s reserve currency rests on trust in US institutions. A politicised Fed would erode that trust. Foreign holders of US dollars will seek to diversify into other currencies and gold. The sell off in US government bonds would be mirrored by a sharp fall in the US dollar, compounding a trend that has already emerged after Trump’s tariff announcements (see Chart 1). In an adverse feedback loop, a weaker US dollar would eventually raise the price of imported goods, stoking inflation and inflation expectations and pushing bond yields higher.